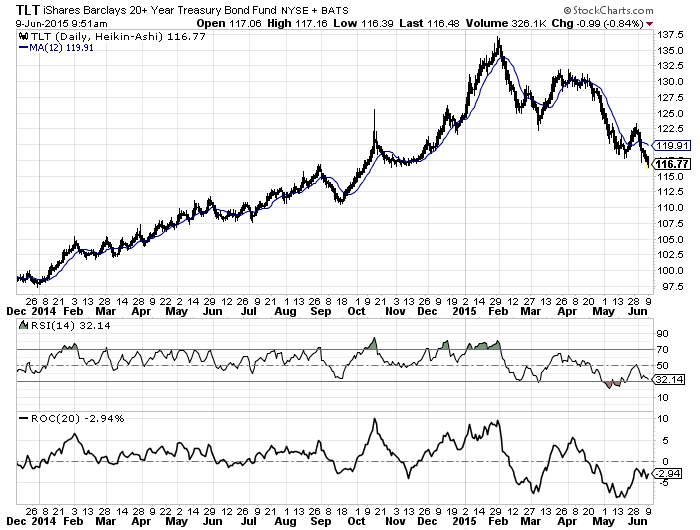

Since taper, non-QE and now int rate rise environment, ROC X 0 has become useful as it was with SPY in QE environment.

I will now change ROC20 link to TLT.

In fact, the numbers may be grossly exaggerated, as some analysts say the real rate of expansion is somewhere on the order of 4% (as opposed to 7%).

We’ve noted on any number of occasions that multiple key indicators — such as rail freight volume, industrial production, electricity consumption, etc. — suggest the dreaded “hard landing” is in fact here, and if Beijing fails to figure out how to balance a sharp decrease in shadow financing with the need to boost credit creation (i.e., if China can’t navigate the impossible task of deleveraging and re-leveraging simultaneously), things could get materially worse before they get better for an economy that’s attempting to mark a very difficult transition from investment-led growth to a consumption-driven model. For more on transparency and why the real rate of growth in China’s economy is “anybody’s guess”, see “Guessing Game: China’s ‘Real’ GDP Growth Could Be As Low As 3.8%.”