Notice on May 1 the utwo moved FIRST then IEF followed.

A key concept is ‘negative wealth effect’.

The XHB downturn leads the economy and leads to ‘negative wealth effect’.

Notice on May 1 the utwo moved FIRST then IEF followed.

A key concept is ‘negative wealth effect’.

The XHB downturn leads the economy and leads to ‘negative wealth effect’.

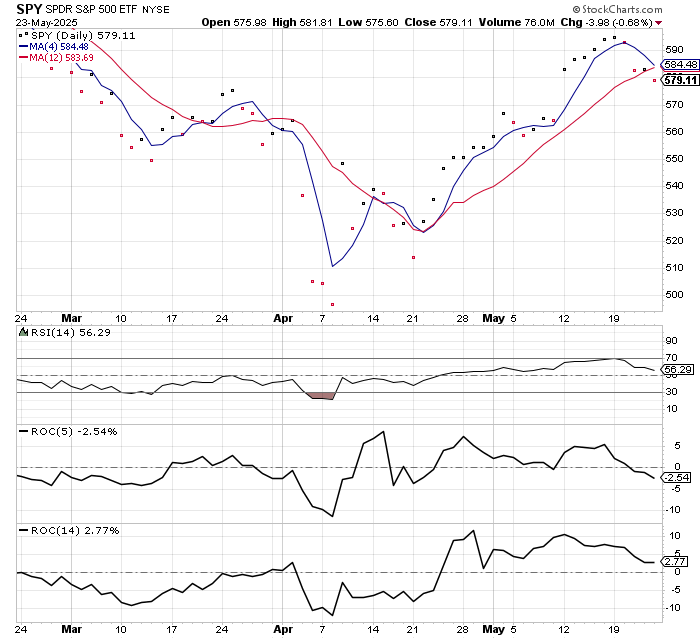

Here you go…OB at 594 on Monday and then began selloff. THIS is a sideways/mild bear market.

No more BULL. THE MARKET DETERMINES THE NEWS NOT THE OTHER WAY AROUND.

Tariffs were also big news in 2018 but did not matter. The ‘deals’ did not materialize and macro problems came to the fore and stocks went down anyway.

Downward pressure on bonds will start to come off with unemployment rate first week of June. Of course, you have 3 days down with bs payroll numbers when hedge funds sell.

However, it’s bought back and more the next week.

AND wall street doesn’t like Mr T budget. I guess the Mr. T magic has worn off.

Once again, it was predicted that 2nd term will be a disaster. Poll ratings are already below 50!

SPY +88 points +17.6%

IEF -2.9 or -2.9% off high so QUITE RESILIENT ! 1/6th…

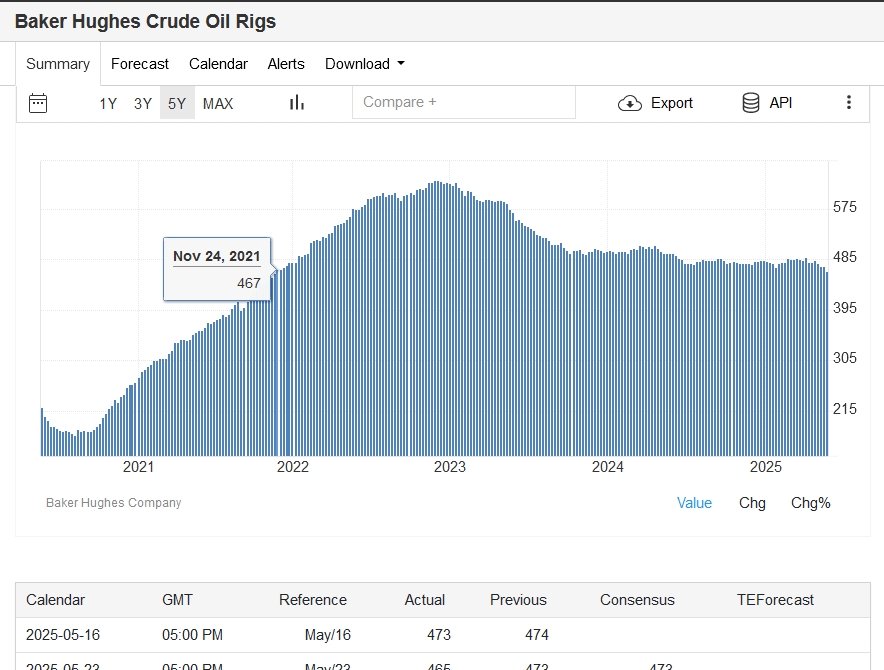

Oil Rigs cracking…I guess the $65 per barrel break even price seems to have merit…

lowest level since Nov 2021…

When IEF remains in negative territory for 4 weeks, the turn around occurs.

Last time was mid-Dec to mid-Jan…waiting for 12dma to cross…

I figured out the youtube guys are real estate agents who take big commission checks when real estate is booming

and switch to gold (also high commission) when real estate turns down!

Not a bad business strategy for sales people though.

Real investors are not on the internet!

The worst is Citibank model at 6.7% unemployment rate. The range for Q1 bank statements is 5-6.7%.

And JPM increased the most by $1B.

To me this is just the beginning…every quarter forecast gets worse and worse from here on out…

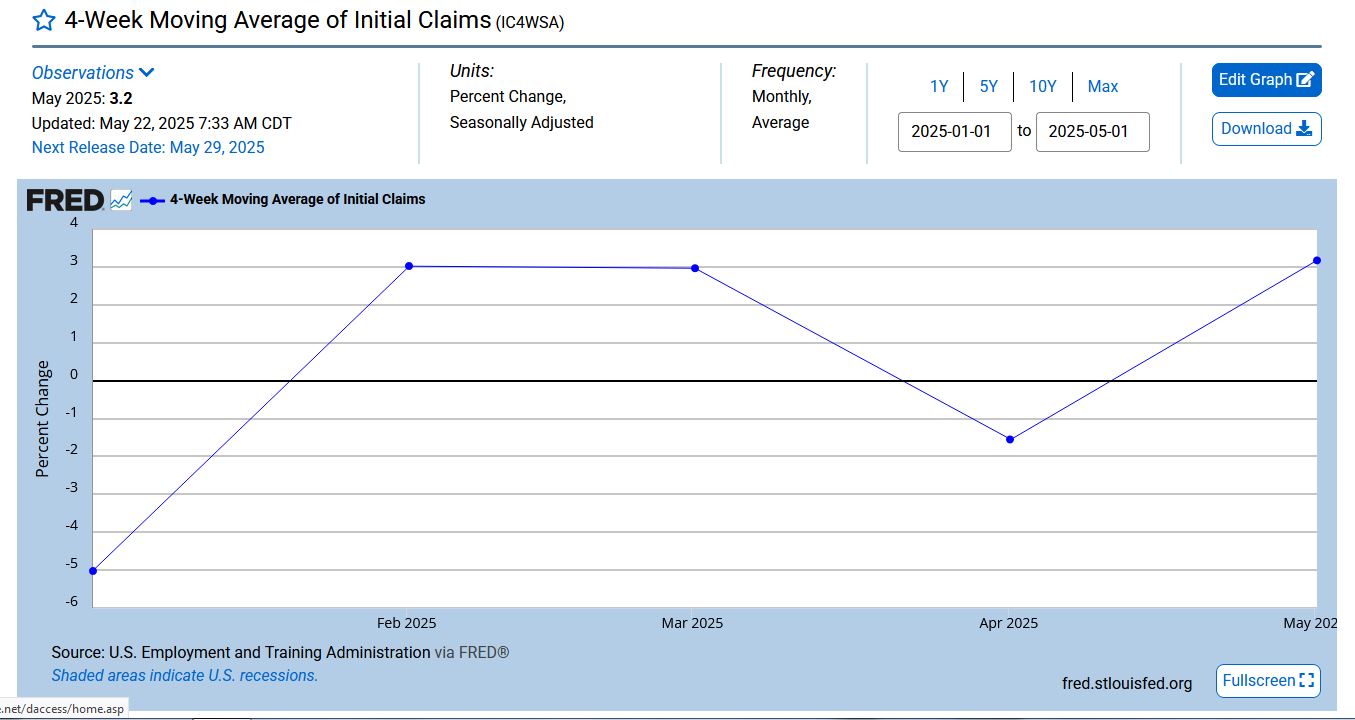

AND claims rise again in May…

And insurance rates +15% California…

Here’s a list of indicators that did not work. after-action report.

Many of these indicators are traditional BUT DID NOT WORK…

Some may work again given that the 50 year super-cycle bubble is bursting.

AND JP has to keep rates high for longer because of his fukups in 2021!!!

Of general background assistance,

What has the last 2-3 years taught us? Don’t listen to perma-bears when risk is ON and vice-versa!

While in Risk Off for the next 2 years, it’s OK to listen to perma-bears.

However, ONCE RISK ON RESUMES AT END OF 2026! DONT LISTEN TO THEM!

Bad numbers will be a problem for 2025-2028…rising unemployment, weak economy etc…

AND REAL ESTATE-SPY will be in the dumps for 5-6 years.

But listening to perma-bears in 2013, was very lethal to GOLD BUGS! In 2013, SPY was the absolute winner and real estate began to move.

This is the basis of the 2Y RULE! No perma-bulls or perma-bears are allowed!

AND all dowm’s are perma-bears with one foot in the grave! I DONT LISTEN TO THEM!

And the opposite is true. When there’s risk on, ignore bad numbers!

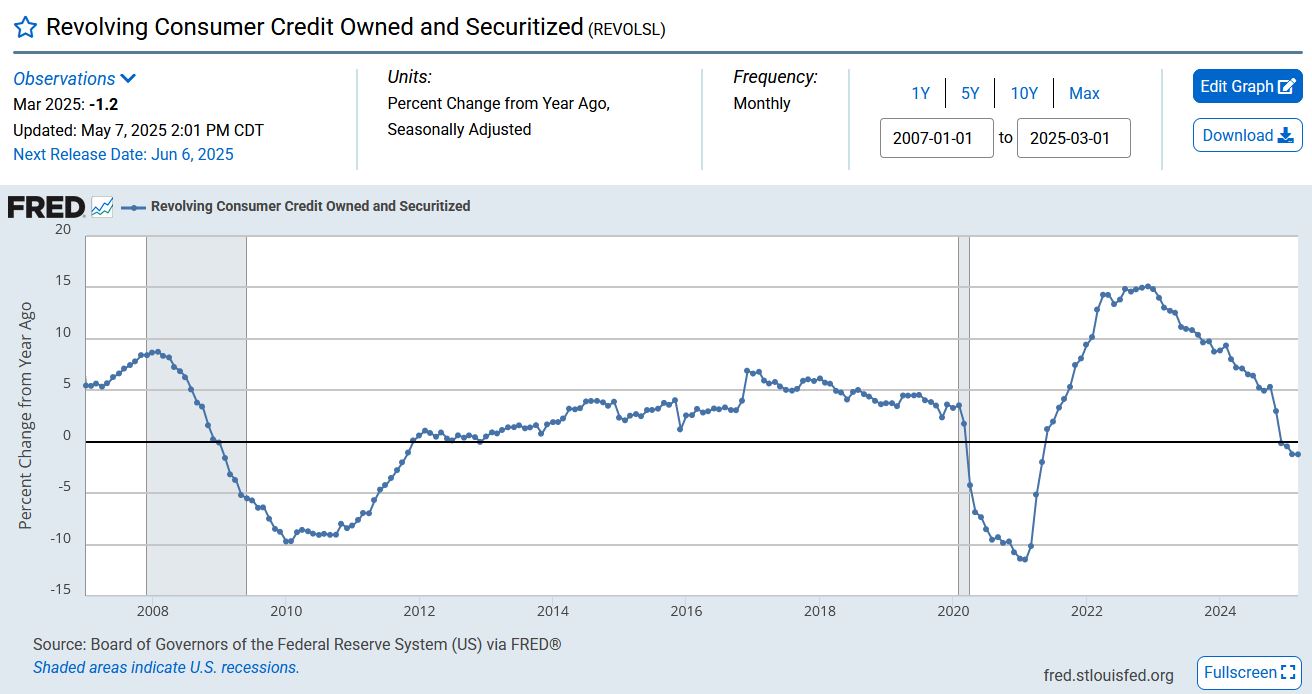

Below indicates that delinquencies are rising faster and faster!!!

Unemployment sentiment continues higher to 70% near record!

Econ numbers get worse for air travel, airlines, and hotels-lodging…

In 2023, they were bad too BUT BUT BUT still RISK ON BACK THEN! DONT MAKE THAT MISTAKE!

AND NOT JUST McDONALDS LOSING…

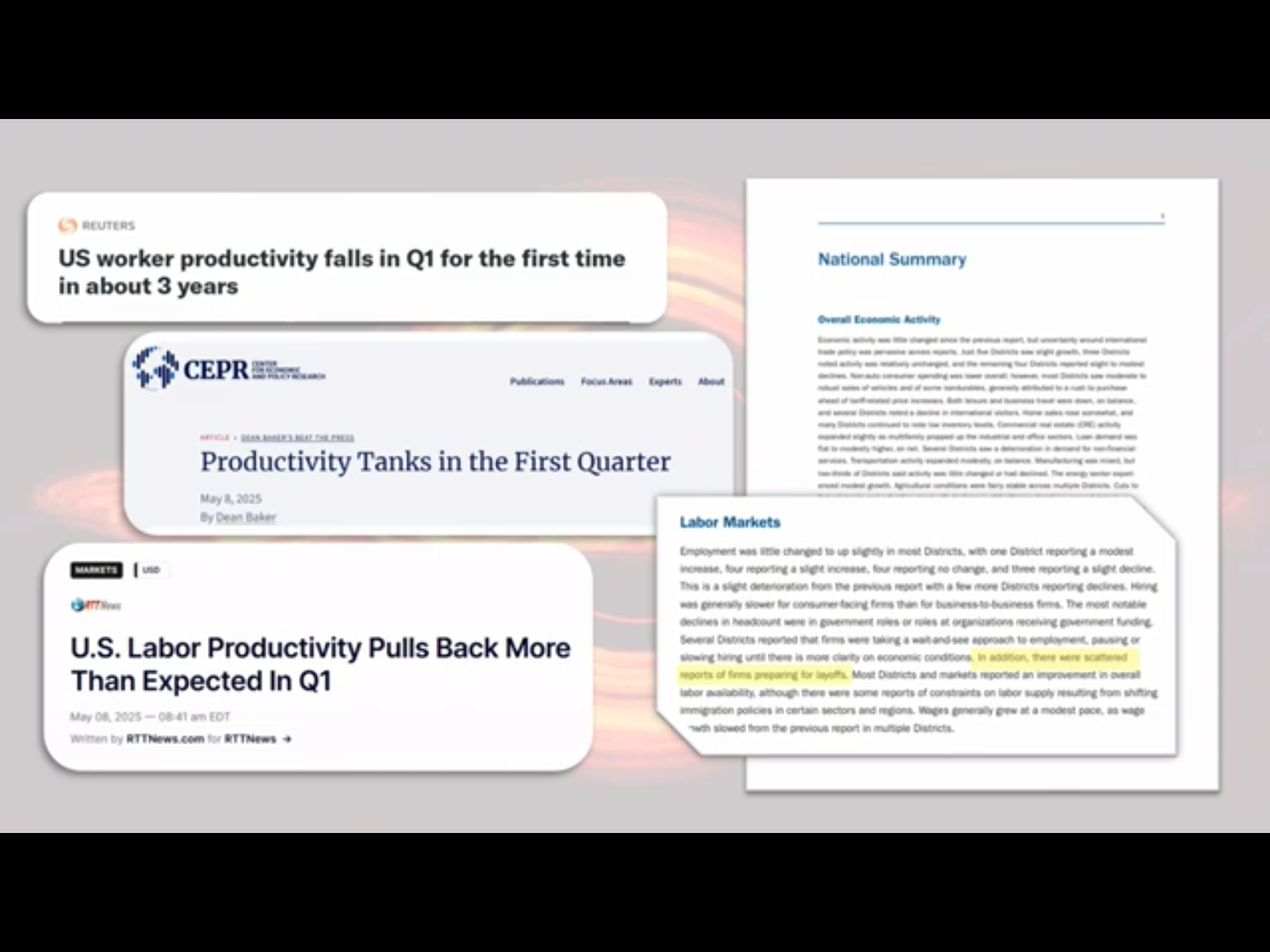

Lastly, productivity worsens so layoffs to come…

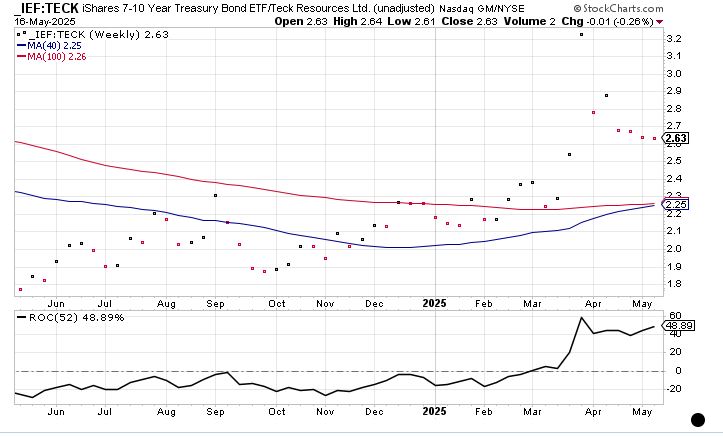

This has been obvious since January…but Teck now has the 40 wkma X the 100 wkma!

Teck is official bear now.

Clearly the 12 wkma told you at the beginning of every year if it was a RISK on or off year….

Best indicators for Risk off/on:

If you look at end of 2022, I called for rise in 2023 of spy +15%….

Teck was clearly ON in 2022 with big rally by April while SPY was crashing…

Good risk on-off chart…..

Mr. T has been told by house members he must ‘pay’ for his tax cut extension.

It’s actually not a tax cut but a tax cut EXTENSION to keep the rate at 37%.

Net stimulus 150B or 0.5% GDP over a year…This is NOT 2017.

Mr. T has decided to raise taxes via tariffs to pay for it.

BUT corps will have to absorb most of this as consumers’ credit cards have been cut off…